- November 15, 2024

- Posted by: lunar1

- Category: cash advance paydayloans

There isn’t any concern one to credit debt is expensive today. Not just manage handmade cards generally incorporate high interest levels, nevertheless current Federal Put aside price nature hikes has resulted in card prices hiking even higher. loan places Sunshine And if you’re carrying an equilibrium on your handmade cards, chances are that you happen to be using a significant amount of attract into the the new charges.

So if you’re making reference to other sorts of debt as well, for example signature loans otherwise student education loans, the present increased rate ecosystem causes it to be costly to pay back what you owe. But the good news would be the fact it does not need to be. There are lots of simple choices for consolidating the money you owe , that could help you save a lot of money when you look at the interest fees over time.

Such as, if you’re a resident having security in your home , you’ve got the option of combining your debts towards the a home collateral mortgage otherwise a home collateral personal line of credit (HELOC) . And you can, doing so you can expect to offer some recovery. However, as with any huge economic circulate, there are lots of crucial benefits and drawbacks so you’re able to consider in advance of bringing it channel.

Straight down rates of interest

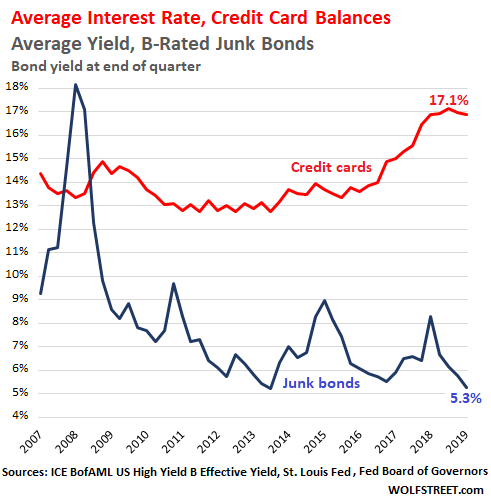

The main advantage of having fun with property security loan or HELOC so you can combine the debt is that household equity finance and you can HELOCs generally have much lower interest levels than just handmade cards or unsecured loans. Instance, at this time, an average rate to your a house security mortgage are 8.59% (since ) and the average HELOC rate is actually nine.04%.

Both prices try considerably less than the common mastercard price , that’s hovering near twenty-two% already. Thus, by rolling your high-focus credit debt for the a lower-rates domestic guarantee financing or HELOC, you happen to be in a position to take advantage of high interest coupons more the life of the financing.

Chance of property foreclosure

Possibly the most significant risk of merging your debt with a home collateral financing otherwise HELOC would be the fact by using your property since equity, you will be getting your residence on the line if you can’t spend the money for repayments in your domestic equity loan. If you find yourself struggling to create your mortgage money, it may possibly trigger property foreclosure, that will be disastrous. This makes it imperative to cautiously determine what you can do while making the, consolidated commission monthly.

Expanded payment months

House guarantee finance routinely have offered payment words than just credit cards otherwise signature loans. Although this tends to make the new monthly premiums a great deal more under control and offer some autonomy regarding your own cost schedule, moreover it means you are in financial trouble for a longer time of your energy.

Settlement costs

Taking out a house security loan otherwise HELOC can come having closing costs , which can add up to hundreds otherwise thousands of dollars, with respect to the bank costs, the quantity your use and other items. These types of upfront costs might be factored into the studies, while the added expense you may negate the potential interest deals in specific things.

Shorter domestic security

All of the buck you borrow against the residence’s guarantee is a buck that is no further accessible to utilize if you prefer they. This may feeling your capability in order to borrow against the residence’s security in the future if you wish to supply money having good small business you’re carrying out, pay for domestic renovations and you may repairs otherwise coverage a unique large debts.

Temptation to help you overspend

After you consolidate your debts to your an individual, lower-interest financing, it can be tempting to begin with accumulating the latest charge card stability again. It’s imperative to break out the cycle away from overspending and be disciplined together with your the payment package. If not, you will be investing in each other your new personal credit card debt and the consolidated obligations each month, which could make challenging financially.

The bottom line

Combining personal debt that have a home guarantee loan is a primary financial choice that needs cautious envision and you can believe. But if complete sensibly, it may be a method to make clear your payments, eliminate interest will cost you and you may really works on getting obligations-free. Just like any biggest monetary choice, in the event, you will need to consider all of your choices to influence new best course of action.

Angelica Leicht are elderly publisher getting Dealing with Your finances, where she writes and you can edits blogs with the a range of personal loans topics. Angelica before kept modifying positions from the Effortless Buck, Interest, HousingWire or any other financial products.