- December 9, 2024

- Posted by: lunar1

- Category: real no credit check payday loans direct lender

Refinancing your home to repay other debt can help you consolidate your balances and possibly save well on notice. Nevertheless includes good dangers, also how many payday loans can you have in Texas it can not the best option if you don’t be eligible for a lower life expectancy rate of interest, or if you’d fight and also make your brand-new payments.

In this article:

- Just how can Refinancing Make it easier to Reduce Costs?

- Ideas on how to Choose Whether or not to Refinance

- Do you require Your house Guarantee in order to Combine Financial obligation?

When you find yourself holding ample financial obligation, it could be tough to pay-off your balance as opposed to delivering particular high step. Refinancing your home to repay your debt is the one option, but it is a shift that accompany tall benefits and you will possible drawbacks that needs to be noticed ahead of time.

Fundamentally, refinancing your home to spend off expense might not be a great wise decision in the event the you are able to struggle to manage your new payments or you will be unable to obtain a good rate on the financial.

Just how can Refinancing Help you Lower Costs?

The main benefit of refinancing their mortgage to pay off obligations is actually saving cash when you look at the desire: Home loan rates are below other kinds of consumer credit like credit cards and personal financing.

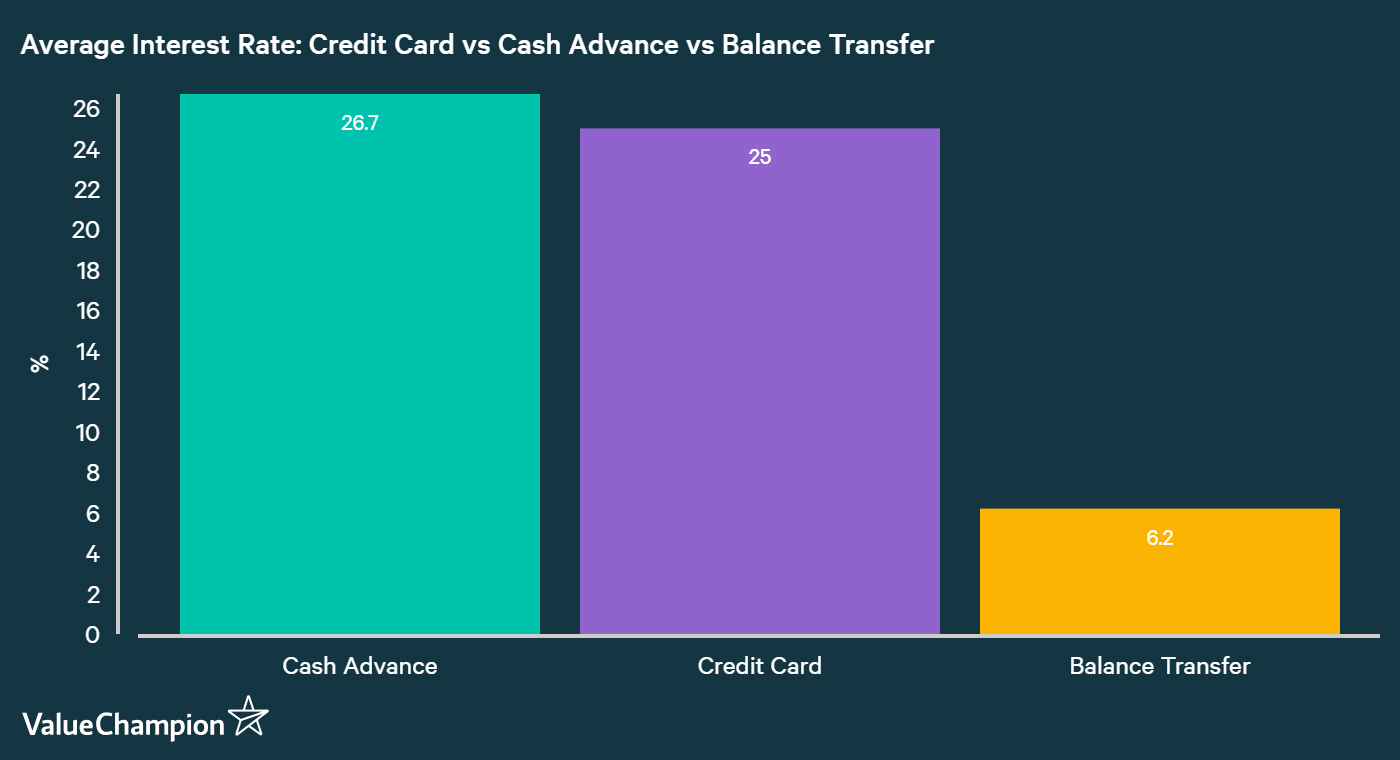

For example, the typical rate of interest into 29-year fixed-speed mortgage loans try six.39% in early May. By comparison, brand new Federal Put aside data listings average rates of interest off % for handmade cards and you will % for 24-few days unsecured loans. Which have People in the us carrying the common charge card and private financing harmony regarding $5,910 and you will $18,255, respectively, predicated on Experian research, it is basic to see exactly how high interest levels throughout these balances accumulates.

- Rate-and-title refinance: An increase-and-term refinance concerns replacement your loan with a new that you to definitely, preferably, sells less interest. New loan also can expose another type of repayment title and you will payment per month amount, but the principal balance remains the exact same. A diminished percentage can give you extra cash you might used to pay down obligations.

- Cash-out re-finance: A cash-away re-finance also functions replacement your mortgage that have a another one, but in this situation, brand new refinance loan are bigger than the remaining harmony on your own mortgage. You can make use of the difference to repay expenses, loans a house repair investment or even for almost every other court mission. That crucial improvement is the fact that the large loan balance usually introduces the general price of the loan, even though you secure a lower price.

The bottom line is: When interest levels try reasonable, a speeds-and-term re-finance can also be take back place on your own finances and also make higher obligations repayments without adding a whole lot more dominant obligations for the home loan. In comparison, a cash-out refinance will provide you with a lump sum payment of money to pay debts, but can enhance your monthly payments.

How exactly to Select Whether to Re-finance

Refinancing have significant effects in your cash, so you should go-ahead carefully before carefully deciding whether to re-finance to help you reduce financial obligation. More critical detail to take on is the current interest rates in your financial and other costs and the latest financial speed you are getting for folks who refinance. Anyway, it creates nothing experience to refinance when the you’ll end up having a somewhat large interest rate.

- Your interest: For folks who qualify for a speeds at least 1% below your home loan speed, a performance-and-identity refinance will make experience. However, a reduced rates lose of lower than 1% is too minimal and also make a meaningful distinction, specially when you cause of settlement costs.

- Your financial obligation top: Refinancing could be worthwhile if your current debt and you can notice rates are highest your harmony is actually broadening somewhat due to help you desire charge. Conversely, a great refinance may possibly not be the most suitable choice in case your loans height is fairly lower-state, a number of thousand bucks otherwise shorter. In this case, after the an obligations fees approach will get suffice to experience your debt.